Roof insurance claim mistakes are avoidable errors that occur when hail damage is documented, inspected, or handled without a clear understanding of how insurance evaluations actually work. In Denver, these mistakes are more common not because homeowners are careless, but because hailstorms often trigger high claim volume, compressed timelines, and overlapping storm dates. That environment rewards speed, not clarity, and small missteps compound quickly.

Most problems start early. Homeowners feel pressure to act, inspections happen before damage is fully understood, and documentation is incomplete or inconsistent. Later, those gaps surface as delayed approvals, scope disputes, or payments that do not match repair realities. The issue is rarely denial. It is process friction created upstream.

This guide explains the most common roof insurance claim mistakes Denver homeowners make after hail and why they matter. You will see how inspection timing, documentation quality, and early decisions influence claim outcomes, not through guarantees, but through predictable insurance systems. The goal is simple: help you understand where mistakes happen so you can avoid them without rushing or guessing.

How Denver Roof Insurance Claims Actually Work After a Hailstorm

Before it makes sense to talk about mistakes, it helps to understand the system those mistakes happen inside. Most frustration around roof insurance claims in Denver does not come from denial or bad intent. It comes from misunderstanding how the process is structured and why it moves the way it does after a hailstorm.

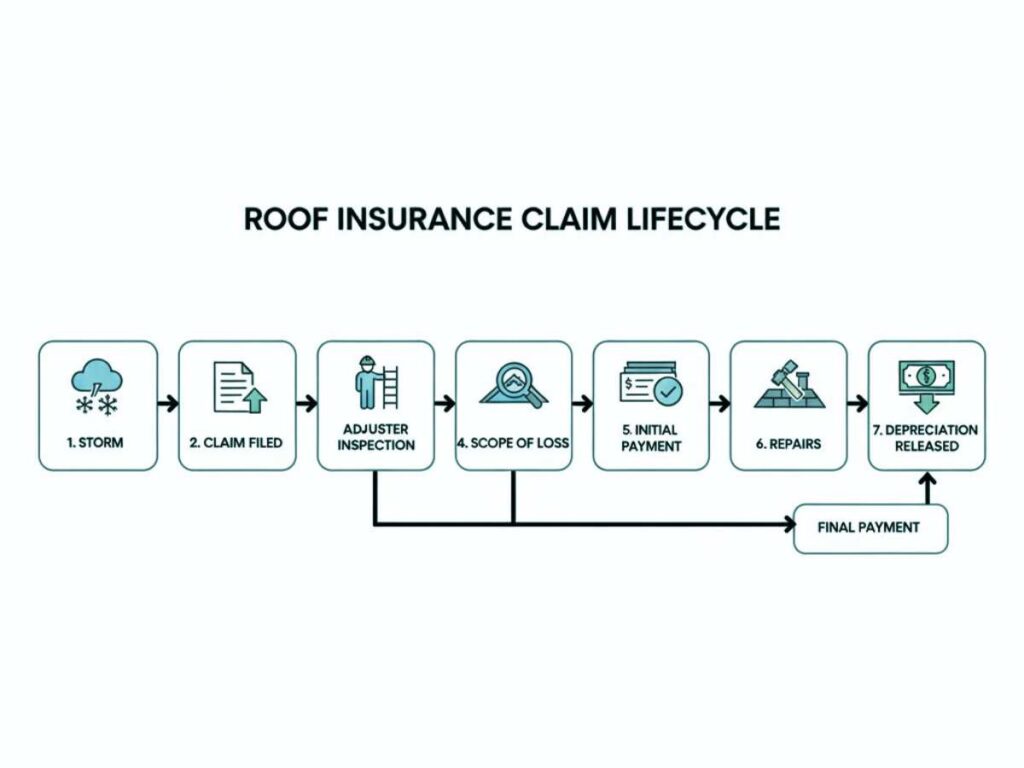

Roof insurance claims move through defined stages, not opinions or negotiations.

Once a claim is filed, it enters a workflow designed to document damage, apply policy terms, and release payment in phases. An adjuster inspection is one step, not a final ruling. Estimates are written based on what can be observed at that moment. Payments follow policy structure, often in multiple releases. None of this happens based on urgency, persistence, or how strongly someone feels about the outcome.

What complicates this in Denver is scale. A single Front Range hailstorm can trigger thousands of claims across multiple carriers within days. That volume changes how insurers operate.

Some delays are volume-driven, not friction-driven. When adjuster schedules back up or inspections are routed through desk reviews or third-party inspectors, the claim is still moving. It is just moving through a system under load. Other delays are friction-driven, caused by missing documentation, unclear storm dates, or scope questions that require clarification. These two delays look similar from the outside, but they have very different causes and solutions.

Denver hail claims also behave differently because storms overlap. Multiple hail events can occur weeks or even days apart, which forces insurers to verify timing, severity, and attribution. That extra verification slows early stages but does not indicate denial or resistance. It is part of how carriers separate one loss event from another.

Here is where misunderstanding creates problems. When homeowners assume the claim should behave like a single yes or no decision, they often react too early. They push back on normal delays, misread partial payments, or treat an initial scope as final. Those reactions are what lead to stalled claims, unnecessary disputes, and avoidable stress later in the process.

Understanding the claim lifecycle first changes how every later decision is made. It turns confusion into context and sets the stage for identifying the real mistakes that actually affect outcomes, especially when you see how hail damage insurance claims typically work in Metro Denver.

Mistake #1: Waiting Too Long to Document Hail Damage After the Storm

After a hailstorm, many homeowners wait before documenting what they see. The roof may look unchanged from the ground, the weather clears quickly, and daily routines take over. In Denver, that delay creates risk. Not because insurance stops caring, but because storm attribution becomes harder the longer documentation is postponed.

Waiting to document hail damage weakens the ability to link roof conditions to a specific storm event. Insurance claims are evaluated based on whether damage can be reasonably tied to a covered event on a known date. When that link becomes unclear, claims often slow down or require additional review steps.

Why Does Storm Timing Matter So Much in Denver?

Yes, storm timing matters more in Denver than in many other regions because hail events often overlap.

Along the Front Range, it is common for multiple hailstorms to occur within the same season, sometimes separated by only days or weeks. When documentation is delayed, adjusters must determine which storm likely caused the damage or whether the condition could predate the reported event. That question does not imply denial, but it does introduce uncertainty into the claim file.

From a system perspective, the issue is not damage severity. It is attribution. Insurance claims are event-based. When the event date is unclear, processing becomes more complex and slower.

How Overlapping Hail Events Complicate Claims

Yes, overlapping hail events increase scrutiny even when damage is legitimate.

When multiple storms affect the same area, insurers rely more heavily on timelines, weather records, and early documentation to align damage with a specific event. If photos, notes, or inspection records are created weeks or months later, adjusters may need additional review to determine whether the damage aligns with the reported storm or a prior one.

This does not mean claims are automatically denied. It means they often require follow-up questions, additional inspections, or internal weather verification. Those steps add time and complexity that could have been avoided with earlier records.

What Kind of Documentation Actually Helps?

Yes, early photo documentation is one of the simplest ways to reduce friction later.

Photos taken soon after the storm help establish baseline condition. Wide shots of roof slopes, closer views of visible impacts, and images of collateral damage such as vents, flashing, or gutters provide context that remains useful throughout the claim lifecycle.

Documentation does not need to be perfect. It needs to be timely. Even basic photos taken safely from the ground can help align roof condition with a specific storm, especially when paired with a clear roof inspection documentation checklist that outlines what adjusters typically look for.

Why This Mistake Leads to Delays, Not Automatic Denials

Waiting to document damage usually leads to delays, not rejection.

When storm attribution is unclear, claims often pause while adjusters verify dates, review weather records, or request additional inspections. That slows approvals and creates frustration for homeowners who expect the process to move faster.

In Denver hail claims, early documentation is less about proving damage and more about preserving clarity. The sooner roof condition is recorded, the fewer questions arise later.

Source context: National Oceanic and Atmospheric Administration storm event data and hail reporting standards

[SOURCE: NOAA Storm Events Database and hail event reporting guidance]

Mistake #2: Filing the Insurance Claim Without a Professional Roof Inspection

After a hailstorm, many Denver homeowners file an insurance claim as soon as damage is suspected. That instinct is understandable. The storm just happened, neighbors are talking, and the claim window feels immediate. The risk is not filing the claim itself. The risk is doing it before there is a clear, independent record of what the roof actually looks like.

This mistake is about sequence, not distrust. Insurance claims move forward based on what is documented at the start. When the first inspection becomes the insurer’s inspection, the claim file is built on whatever damage is visible and recorded during that initial visit.

Why Inspection Order Matters in a Denver Hail Claim

Yes, inspection order affects how completely damage is captured.

In Denver, adjuster inspections often happen under time pressure, especially after widespread hail events. Adjusters are tasked with documenting visible, policy-relevant damage efficiently. That does not mean damage is ignored. It means the inspection is scoped to what can be reasonably identified during that visit.

A professional roof inspection completed before the adjuster visit creates a baseline. It documents damage patterns, roof sections, and collateral impacts while conditions are fresh. That information does not override the adjuster’s findings, but it helps ensure the adjuster is evaluating the full picture rather than discovering issues later, which is why many homeowners choose to start with a professional roof inspection before the adjuster visit.

From a system perspective, the difference is simple. Early documentation keeps the claim in evaluation mode. Late discoveries push the claim into correction mode.

How Insurer-First Inspections Can Miss Damage Patterns

Yes, some damage patterns are easy to miss without a focused inspection.

Hail damage is not always uniform. Certain slopes, exposures, or materials take impact differently. Granule loss, shingle bruising, or fractures can be subtle, especially when viewed quickly or from limited access points.

When those patterns are not identified early, they often surface later during contractor review or repair planning. At that point, the claim has already moved forward with an initial scope. Any newly identified damage must be justified through supplements, re-inspections, or additional review.

This does not mean coverage is denied. It means the process becomes slower and more complex.

Why This Mistake Leads to Supplements and Delays

The core consequence of skipping a professional inspection is scope lock-in.

Once an initial scope of loss is written, every missed item has to be explained, documented, and approved after the fact. That shifts the claim from straightforward assessment into revision and verification. Each revision adds time, additional review, and more back-and-forth between parties.

In Denver hail claims, that extra friction is common, but it is not inevitable. Early, independent documentation helps the claim start with a clearer foundation, which reduces the need for corrections later.

The takeaway is not that homeowners should delay filing a claim. It is that documentation sequence matters. A clear inspection record at the beginning preserves clarity throughout the claim lifecycle and reduces avoidable delays once the process is underway.

Mistake #3: Treating the Adjuster Visit Like a Negotiation

When the adjuster arrives, many homeowners feel pressure to explain, defend, or convince. The visit can feel like a meeting where the outcome depends on saying the right things. That framing is understandable, but it misunderstands how the process actually works. An adjuster visit is not a negotiation. It is a documentation exercise governed by standards, not persuasion.

This mistake does not come from bad intent. It comes from assuming the adjuster has discretion to be talked into outcomes. In reality, adjusters work inside a structured system that limits how decisions are made.

Is the Adjuster Visit About Persuasion or Evidence?

No, the adjuster visit is not about persuasion. It is about evidence.

Adjusters are responsible for documenting observable damage and applying policy criteria to what they can verify. They are not there to debate repair methods, argue coverage, or weigh competing opinions during the inspection itself. Their role is to collect information that can be reviewed, measured, and supported later.

From a system standpoint, spoken explanations carry far less weight than physical evidence. Photos, measurements, damage patterns, and consistency across roof sections are what shape the claim file. Persuasive language does not substitute for documentation, and it does not override policy terms.

When inspections turn into persuasion attempts, the usual result is not denial but a narrower initial scope, more follow-up questions, and a higher likelihood that missed areas have to be addressed later through re-inspection or supplemental review.

How Homeowner Statements Are Recorded

Yes, homeowner statements can become part of the claim record.

Adjusters often note what homeowners say during inspections, especially when it relates to timing, prior condition, or observations. These notes are not meant to trap anyone, but they do become part of how the claim is evaluated.

Casual comments can introduce uncertainty without the homeowner realizing it. Saying you are not sure when damage happened, mentioning older issues without context, or speculating about roof condition can complicate storm attribution or damage classification later. Once recorded, those statements may require clarification or follow-up to resolve.

This is why clarity matters more than commentary. Sticking to what you observed, when you observed it, and what changed after the storm keeps the record clean.

Why Negotiation Framing Slows Claims

The biggest risk of treating the visit like a negotiation is that it shifts focus away from documentation.

When homeowners try to persuade, they often talk more than they show. Meanwhile, the adjuster’s process continues based on what can be documented visually and consistently. Any mismatch between spoken claims and recorded evidence creates friction that has to be resolved later through review or supplemental documentation.

In Denver hail claims, that friction usually shows up as delays rather than denials. Additional inspections, follow-up questions, or requests for clarification slow the process without changing the underlying facts.

The more productive approach is simple. Treat the adjuster visit as an inspection, not a discussion. Evidence carries the claim forward. Conversation does not.

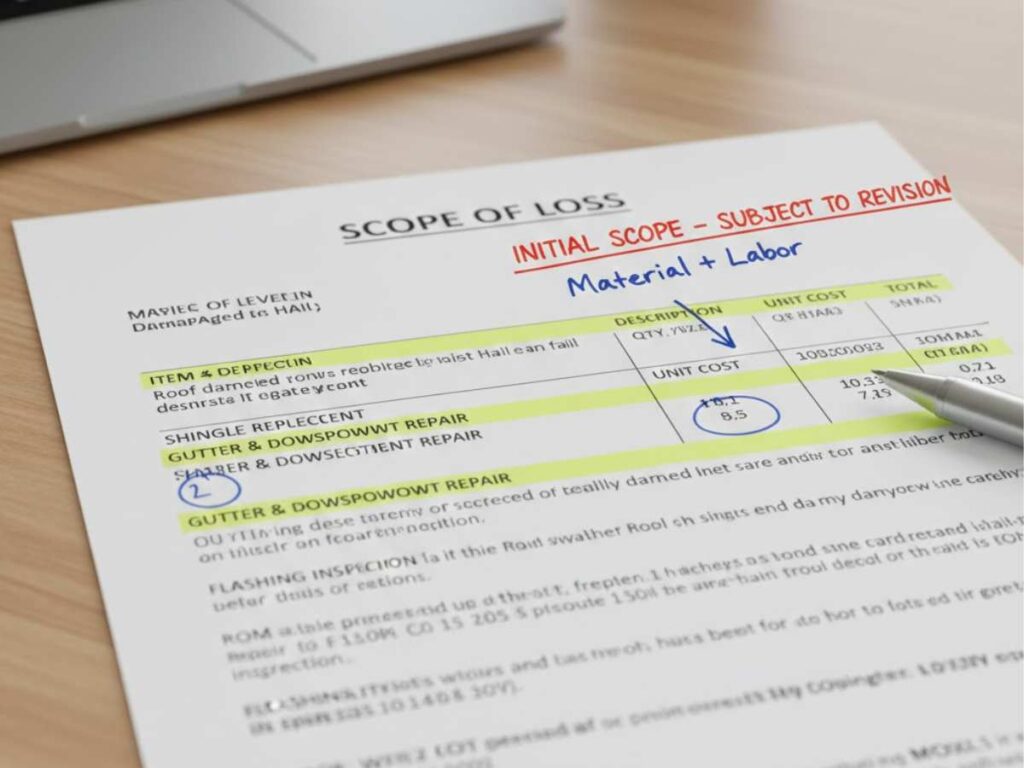

Mistake #4 — Misunderstanding the Scope of Loss as Final Approval

After the adjuster visit, the scope of loss often feels like a finish line. It arrives as a formal document, it includes dollar amounts, and it looks definitive. For many Denver homeowners, this is the moment they assume the claim is settled. That assumption is one of the most common reasons claims slow down later.

The scope of loss is not a final approval. It is an early snapshot based on what was visible and documentable at the time of inspection.

Is the Scope of Loss the Final Insurance Decision?

No, the scope of loss is not final approval.

It reflects what the insurer agrees to cover based on a surface-level inspection and the information available at that moment.

Adjusters document visible damage, apply policy terms, and produce a scope that allows the claim to move forward. They are not confirming that every damaged component has been identified. In Denver hail claims, that distinction matters because many issues are not visible until materials are removed.

From a system perspective, the scope functions as a working document. It establishes an initial repair framework, not the full extent of what may ultimately be required.

Why the Scope Is a Snapshot, Not a Blueprint

Yes, the scope is intentionally limited by timing and access.

Adjuster inspections happen before tear-off, before underlayment is exposed, and before code requirements are fully evaluated.

That limitation is not an error. It is how the process is designed to function. Insurers approve what can be confirmed early, then revise when new information becomes available. In Denver, where hail damage often affects multiple roof layers, this staged approach is common.

The problem arises when homeowners treat the initial scope as complete and irreversible. When that happens, legitimate revisions feel like disputes instead of routine claim evolution.

What Items Are Commonly Missing From the Initial Scope?

Yes, missing items are common, especially on hail-damaged roofs.

These omissions usually surface once work begins and concealed conditions are visible.

Common examples include underlayment damage, flashing issues, ventilation components, or code-required upgrades that were not identifiable during a surface inspection. These items are typically addressed through claim revisions, not denials.

When homeowners expect the first scope to cover everything, these additions feel unexpected. In reality, they are part of how the claim lifecycle accounts for limited early visibility.

How This Mistake Creates Delays Later

The consequence of misunderstanding the scope is usually delay, not underpayment.

When homeowners assume the scope is final, repairs may pause while approvals catch up, which can delay construction scheduling and depreciation release. Contractors may hesitate to proceed without clarification. Insurers may need additional documentation before authorizing revisions. All of this slows progress even when coverage is appropriate.

For homeowners navigating this stage, understanding how underpaid or disputed roof claims are typically addressed can clarify what steps exist when a scope needs revision and why that process is procedural rather than adversarial.

Understanding the scope as a starting point rather than an endpoint preserves momentum. It allows revisions to be handled as expected steps instead of perceived setbacks.

In Denver hail claims, clarity about the scope of loss does not change coverage. It changes expectations. That difference alone prevents many avoidable delays.

Mistake #5 — Misunderstanding ACV, RCV, and Depreciation Payments

After the adjuster visit, many Denver homeowners assume the hardest part of the claim is over. Then the first insurance check arrives and the number feels wrong. This moment causes more confusion and frustration than almost any other stage of a hail claim, not because something went wrong, but because payment structure is often misunderstood.

The issue is not approval. It is how roof claims are paid.

Why the First Insurance Check Often Looks Low

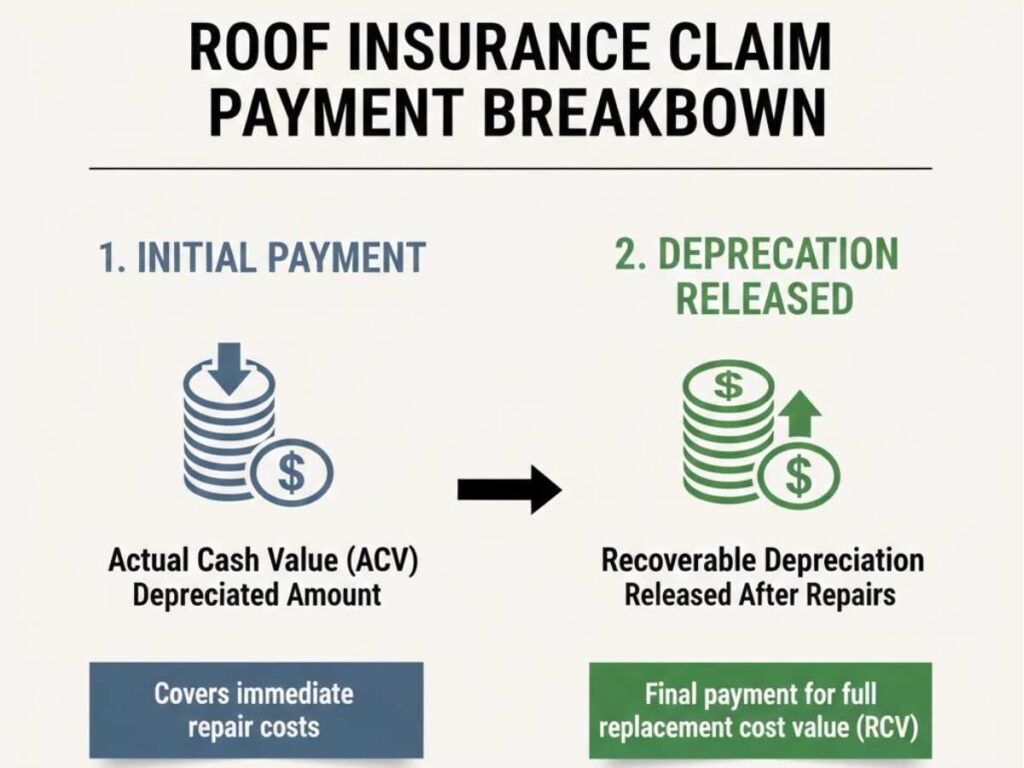

Yes, the first insurance payment is usually lower than the total repair cost because most policies release funds in stages.

In Colorado hail claims, insurers typically pay roof damage using one of two policy structures: Actual Cash Value or Replacement Cost Value. Both rely on depreciation, which is where most confusion begins.

Actual Cash Value, or ACV, reflects the roof’s age and condition at the time of loss. Depreciation is deducted upfront, and no additional payment is issued later. Replacement Cost Value, or RCV, works differently. Under an RCV policy, the insurer initially pays the depreciated amount, then holds back depreciation until repairs are completed and documented.

That means the first check is not designed to cover the full replacement cost. It is meant to start the process.

How Two-Stage Roof Claim Payments Actually Work

Yes, most Denver hail claims follow a two-stage payment process under RCV coverage.

The first payment reflects the approved scope of loss minus depreciation and the deductible. The second payment releases withheld depreciation after the roof work is completed and invoices are submitted, which is why depreciation is typically issued only once roof replacement work is completed and documented.. This structure allows insurers to confirm that repairs were actually performed before issuing the remaining funds.

This system is procedural, not adversarial. It applies even when damage is clear and coverage is valid.

When homeowners assume the first check is final, repairs often stall, timelines stretch, and claim files stay open longer than necessary.

Why This Mistake Creates Delays, Not Denials

Misunderstanding ACV, RCV, and depreciation does not usually cause a claim to be denied. It causes hesitation.

Homeowners may pause repairs, wait for additional payments that are not yet due, or assume something was missed in the inspection. That uncertainty slows coordination between contractors, lenders, and insurers. In Denver, where hail claims already move through volume-driven workflows, those pauses add unnecessary friction.

Understanding payment structure early helps set realistic expectations, keeps the project moving, and prevents avoidable frustration later in the claim.

Source relevance: Insurance policy payment structures and depreciation handling

[SOURCE: Policy structure explanations from state insurance departments or standard homeowners policy forms]

Mistake #6 — Assuming Supplements Mean the Claim Is Failing

After the first approval, many Denver homeowners feel a sense of relief. The inspection is done, paperwork arrives, and work seems ready to move forward. When a supplement is introduced later, that relief often turns into concern. It can feel like something went wrong or that the claim is being reopened because of a problem. In reality, supplements are a normal part of how roof claims function, especially after hailstorms along the Front Range.

Yes, supplements are routine in Denver hail claims and do not signal that a claim is failing.

A supplement is simply a request to revise the scope of loss after additional damage is identified during repairs. Roof inspections happen from the surface. Once work begins, concealed conditions often become visible. That is not an exception to the process. It is how the process is designed to work.

Why Are Supplements Common After Denver Hailstorms?

Yes, supplements are more common in Denver because hail damage often affects roof systems in layers.

Hail can fracture shingles, loosen fasteners, or compromise underlayment in ways that are not visible during an initial inspection. Adjusters document what can be confirmed at the time of the visit. Contractors discover additional issues only after removing materials and accessing areas that were previously covered.

From a system standpoint, this is expected. The initial scope is written as a snapshot based on observable conditions. The supplement updates that snapshot once real repair conditions are known.

What Types of Damage Usually Trigger Supplements?

Yes, supplements often relate to damage that could not be verified during the first inspection.

Common examples include damaged underlayment, flashing issues around vents or chimneys, decking problems, or code-related requirements that only become clear during teardown. These items are not added because the original inspection was careless. They are added because access was limited at that stage.

This distinction matters. A supplement reflects new information, not a reversal of the claim decision.

How Do Supplements Affect Claim Timelines?

Yes, supplements usually extend timelines slightly, but they rarely reset the claim.

When a supplement is submitted, the insurer reviews the additional documentation and revises the scope or payment if the damage aligns with policy terms. That review takes time, typically days or a few weeks, depending on volume and documentation quality.

The key point is this. Supplements add steps, not friction. They slow the process in a predictable way, not an adversarial one. Claims that include supplements are still moving forward. They are just being updated to reflect the full condition of the roof.

Why Assuming Supplements Mean Trouble Causes Unnecessary Stress

The mistake is not the supplement itself. It is the assumption that something has gone wrong.

When homeowners view supplements as a failure signal, they often pause decisions, delay repairs, or worry that approval is at risk. In reality, a supplement usually means the claim is being refined to better match actual roof conditions. Understanding that difference helps keep expectations grounded and prevents misreading a normal step as a negative outcome.

Mistake #7 — Overlooking Mortgage or Lienholder Endorsement Delays

Once a roof insurance claim is approved, many Denver homeowners expect the process to be essentially finished. When the check arrives but repairs still cannot begin, confusion sets in. In most cases, the delay has nothing to do with insurance decisions or damage disputes. It comes from how mortgage companies and lienholders control insurance funds after approval.

Why checks get delayed after approval

When a mortgage or lien is attached to a property, the lender is often listed on the insurance check. This gives the lender a legal interest in how claim funds are used. Before money can be released for repairs, the lender typically requires endorsement, documentation, or escrow handling.

From a system perspective, the delay happens after the insurer has already completed its role. The claim is approved, payment is issued, and coverage is no longer in question. The bottleneck occurs because the lender must verify that repairs will protect the property that secures the loan. This review process varies by lender and is often administrative rather than technical, which is why timelines can feel unpredictable.

What homeowners can and cannot control

Homeowners cannot bypass lender endorsement requirements when a mortgage or lien is involved. Those procedures are set by the lender and apply regardless of contractor, insurer, or claim size.

What homeowners can control is preparation. Understanding early that endorsement may be required helps set realistic expectations for repair timing. Providing requested documents promptly and asking the lender about their specific release process can reduce idle time once the check is issued. What does not help is assuming the claim is stalled or disputed. In most cases, the delay reflects payment control rules, not claim problems.

The practical consequence of overlooking this step is scheduling friction. Roof repairs may need to wait until funds are cleared, even though the claim itself is complete. Recognizing lender involvement as a separate system prevents unnecessary frustration and keeps expectations aligned with how Denver roof claims actually conclude.

Source context: Lienholder endorsement and escrow procedures outlined in standard mortgage servicing guidelines and insurance payment handling practices

[NEEDS SOURCE: Lienholder payment procedures]

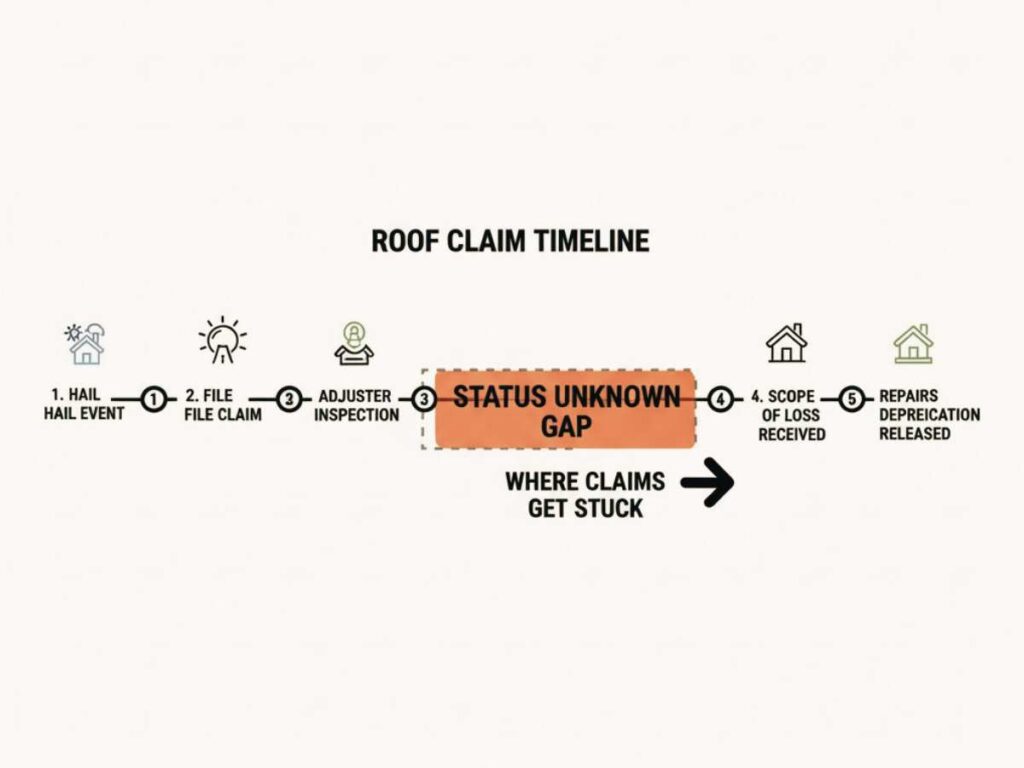

Mistake #8 — Letting the Claim Go Quiet Without Clarifying Status

After an inspection or document submission, it is common for a roof insurance claim to go quiet. Days pass. Sometimes weeks. In Denver, that silence is not automatically a problem, but it is also not something to ignore indefinitely. The mistake is assuming that no news always means progress is happening in the background.

The key is understanding the difference between normal backlog and actual stagnation.

Backlog vs. Stagnation Are Not the Same Thing

Yes, claims can be quiet because of volume, but that does not mean every delay is harmless.

After major hail events in Metro Denver, insurers often process thousands of claims at once. During these periods, adjusters may be waiting on internal review queues, engineering sign off, or supplement evaluation. That kind of delay is volume driven. It usually resolves once the file reaches the next review stage.

Stagnation is different. A stalled claim is one where the next step is unclear, missing, or undocumented. This can happen when requested information was never received, when a supplement is pending review without confirmation, or when the file is waiting on clarification that was never formally logged.

From a system standpoint, backlog is passive. Stagnation is procedural.

Why Unchecked Silence Creates Real Consequences

Yes, letting a claim stagnate can quietly extend timelines beyond what homeowners expect.

When a claim sits without a clearly documented status, it often loses momentum inside the insurer’s workflow. Files may fall out of active queues, require re review, or be reassigned. That can delay key steps such as supplement approval, depreciation release, or final payment processing.

The consequence is usually not denial. It is delay caused by lost context. When a file has to be reactivated later, adjusters may need to re verify dates, documents, or inspection findings that were already reviewed once. That repetition adds time that could have been avoided with a simple status clarification earlier.

When to Request a Written Status Update

Yes, requesting a written update is appropriate when silence extends beyond normal processing windows.

A status request is not a complaint. It is a way to anchor the claim’s position in the system. Asking whether the file is pending review, awaiting documentation, or queued for payment helps prevent assumptions on both sides.

Written updates matter because they create a timestamped record. That record helps ensure the claim remains active and reduces the risk of procedural drift as weeks pass. In Denver hail claims, this step often separates files that move steadily forward from those that quietly stall.

The goal is not to accelerate the process artificially. It is to make sure the process is still happening at all.

What to Do If You’ve Already Made One of These Roof Claim Mistakes

Realistically, many Denver homeowners recognize these mistakes only after a claim feels slow, confusing, or stuck. That moment often comes when communication drops off, an estimate seems incomplete, or a payment does not arrive when expected. The important thing to understand is this: most roof insurance claim mistakes do not permanently derail a claim. They usually introduce friction, not failure.

Insurance claims are not static decisions. They are working files that can be clarified, updated, and corrected when new information is added.

Are roof insurance claim mistakes fixable after the process starts?

Yes, many roof insurance claim mistakes are fixable if documentation and communication are corrected.

Missed documentation, delayed photos, or early misunderstandings typically affect clarity, not eligibility. When new evidence is provided, insurers often re-evaluate portions of the claim. This can include revised scopes of loss, supplemental inspections, or additional payment review.

From a system perspective, insurers are not reopening claims out of generosity. They are responding to improved information. When documentation becomes clearer, the claim becomes easier to process.

The practical consequence of fixing mistakes later is usually time. Corrective steps often extend review cycles by weeks rather than days, especially during heavy Denver hail seasons when adjuster workloads are already high.

How can momentum be restored if a claim has slowed down?

Yes, momentum can often be restored by re-establishing clarity rather than escalating conflict.

Claims stall most often when the file lacks a clean narrative. Restoring momentum means identifying where clarity was lost and correcting that specific gap. Common examples include providing dated photos that tie damage to a specific storm, documenting previously missed roof components, or requesting written confirmation of claim status.

This is also where understanding process boundaries matters. Homeowners can request explanations, status updates, and documentation reviews. They cannot force outcomes or bypass insurer review steps. When expectations stay aligned with how claims actually move, progress tends to resume more predictably.

The goal at this stage is not speed. It is coherence. Claims move faster when fewer questions remain unanswered.

When does correction become harder?

Yes, corrections become harder when time gaps grow and records remain incomplete.

The longer a claim sits without updated documentation or clear follow-up, the more review steps may be required later. That does not mean denial is likely. It means approvals and payments may shift into later processing windows or require additional internal review.

This is why timely clarification matters even after a mistake is recognized. Restoring clarity earlier limits how much extra time the correction phase adds.

The central takeaway is calm but deliberate action. Most Denver roof insurance claim mistakes do not end claims. They slow them. Correcting them works best when homeowners focus on documentation quality, written communication, and understanding where the claim sits in the insurer’s process rather than assuming the opportunity has passed.

How to Avoid Costly Roof Insurance Claim Mistakes in Denver

Before moving to next steps, it helps to pause and lock in what actually drives outcomes in Denver hail claims. These takeaways are not tactics or shortcuts. They reflect how the system evaluates damage, timing, and payment.

- Early documentation protects clarity, not approval. Photos and notes taken soon after a hailstorm make it easier to tie damage to a specific event in a region where storms often overlap. Delays usually lead to extra review, not instant denial.

- Insurance claims move in stages, not decisions. Initial inspections, scopes of loss, depreciation payments, and supplements are all part of a sequence. Treating any single step as final often creates confusion.

- First checks are rarely the full picture. Replacement Cost Value policies commonly release depreciation only after repairs are completed, which is why early payments often look lower than expected.

- Supplements are routine in Denver hail claims. Additional damage discovered during repairs does not mean the claim is failing. It usually means the file is being updated to reflect conditions that were not visible at inspection.

- Silence creates risk, not patience. When a claim goes quiet, the safest move is to request a clear written status update so backlog delays do not turn into stalled files.

These points form the baseline. When homeowners understand them, the rest of the claim process becomes easier to evaluate without panic or second guessing.

How Denver Homeowners Can Protect Their Roof Claim After Hail

Roof insurance claim mistakes in Denver are rarely about doing something wrong. They are procedural, not personal. Most happen because homeowners are forced to make decisions quickly, with incomplete information, after a disruptive hail event. The system is unfamiliar, the terminology is dense, and timelines feel unclear. That combination creates friction, not failure.

What consistently matters more than speed is preparation. Early documentation, clear inspection records, and an accurate understanding of how scopes, depreciation, supplements, and payments actually work do more to protect a claim than rushing to file or pushing for fast answers. When those pieces are in place, claims tend to move through predictable stages, even if they take time.

Denver hail claims also behave differently than storm claims in many other regions. High claim volume, overlapping storm dates, and layered review processes are normal here. When homeowners understand that structure, delays feel less personal and decisions become easier to evaluate. The goal is not to control the process, but to understand it well enough to avoid preventable mistakes.

A roof claim does not need to be perfect to be successful. It needs to be clear, documented, and allowed to move through the system as designed. When that happens, outcomes are usually steadier and far less stressful, even in a hail-heavy market like Denver.

Storm and Insurance Reference Sources

- National Oceanic and Atmospheric Administration (NOAA) – Storm Events Database

https://www.ncdc.noaa.gov/stormevents/National Oceanic and Atmospheric Administration (NOAA) – Storm Events Database - Colorado Division of Insurance – Homeowners Insurance and Claims Overview

https://doi.colrado.gov/insurance-products/homeowners-insurance - National Association of Insurance Commissioners (NAIC) – Homeowners Insurance Guide

https://content.naic.org/consumer/homeowners-insurance - Fannie Mae Servicing Guide – Insurance Loss Proceeds

https://servicing-guide.fanniemae.com/1026076351

Recent Comments