A roof insurance claim process is the sequence of steps a Colorado homeowner follows after storm damage to document the loss, work through the insurer’s inspection and pricing review, and collect payment for repair or replacement. The terminology alone creates confusion the first time through: Xactimate, ACV, RCV, SB 38, scope of loss, recoverable depreciation. The sequence matters in ways that are not obvious until something goes wrong. A homeowner who calls the insurer before a contractor has inspected the roof hands the adjuster the ability to close the scope of loss before the contractor can dispute it.

The complete eight-step process runs from initial roof inspection through final depreciation payment. It covers what the adjuster does on the roof, how the scope of loss drives the initial payout, where supplemental payments originate, and what contractor selection under CRS 6-22-101 through 6-22-105 requires.

Roof Insurance Claim Process in Colorado: What to Expect

Colorado roof insurance claims follow a defined sequence that most homeowners encounter once, without preparation. Carriers operating in Colorado process a high volume of hail claims relative to most other states, which makes adjuster workflows routine on the carrier side. In Metro Denver, a straightforward hail damage claim runs 30 to 90 days from first inspection to final depreciation payment. Claims that stretch past 60 days typically involve a disputed scope, a supplement negotiation, or a mortgage company endorsement requirement.

Colorado operates under SB 38, codified as CRS 6-22-101 through 6-22-105, which governs every roofing contract tied to an insurance claim. That statute changes how contractor selection works and what the signed contract must contain. It is one reason Colorado claims move differently than claims in states without residential roofing consumer protection law.

The single most common error Metro Denver homeowners make is calling the insurance carrier before a contractor has inspected the roof. Once the claim is filed without documented contractor findings, the adjuster writes the initial scope without that input. Supplementing later is possible but harder.

How a Colorado Roof Insurance Claim Works: 6-Step Overview

- Inspect — A licensed roofing contractor inspects the roof, documents hail and wind damage, and produces a written report before filing.

- File — The homeowner contacts the carrier with the policy number and date of loss and receives a claim number and adjuster assignment.

- Adjuster assigned and inspection completed — A staff or independent adjuster inspects the roof, marks test squares, counts impacts per slope, and enters findings into Xactimate.

- Scope of loss issued — The adjuster produces a line-item Xactimate estimate. The contractor reviews it for missed slopes, code components, and pricing.

- ACV payment issued and supplement submitted if needed — The carrier releases the initial actual cash value payment after subtracting depreciation and the deductible. The contractor submits supplements for missed items.

- Closeout and depreciation recovery — After municipal inspection, the contractor submits the certificate of completion and final invoice, and the carrier releases recoverable depreciation.

The eight detailed sections below treat each stage in full.

Step 1: Inspect and Document Roof Damage Before Filing

Before calling the carrier, get a licensed roofing contractor on the roof. The documentation that inspection produces becomes the foundation the entire claim is built on. Filing without it means the adjuster writes the initial scope without contractor input on record, and disputing or supplementing it later starts from a weaker position.

Homeowner self-inspection misses most qualifying damage. Hail impact on asphalt shingles does not always look like visible breakage from the ground. What carriers’ adjusters identify, and what Haag Engineering damage assessment criteria formalize, is hail bruising: a soft depression where the granule layer has been displaced and the underlying fiberglass substrate compromised. From the ground, most homeowners see surface marks and underestimate scope.

Haag-certified inspectors carry additional weight. Haag Engineering developed the methodology most carriers reference, so a Haag-certified report disputes adjuster findings on the adjuster’s own terms. Soft-metal damage on flashing, gutters, downspouts, and vent caps is the corroborating evidence that strengthens a claim when shingle damage is disputed the same hailstorm that bruised shingles will dimple aluminum gutters, and that pattern is difficult for a carrier to attribute to wear.

The pre-filing inspection also establishes a record of the damage condition tied to the original storm event. Without it, connecting later-observed damage to the original loss becomes a question the carrier does not have to resolve in the homeowner’s favor.

What the Contractor’s Inspection Report Should Include

- Photo log with dated images of impact sites on each slope, labeled by section

- Test square documentation: chalk-marked impact sites within a measured 10-by-10-foot section, with impact count recorded per slope

- Slope diagram identifying which roof faces sustained qualifying damage

- Soft-metal evidence: photos of hail dimpling on gutters, flashing, vent caps, and downspouts

- Written damage summary including estimated date of loss, storm event, materials affected, and claim threshold assessment

[Haag Engineering damage assessment standards]

Step 2: File the Claim With Your Insurance Carrier

The claim filing call is a data exchange, not a damage assessment. The carrier’s representative is collecting information to open a file and assign an adjuster. Volunteering damage estimates or speculating on cause creates a record the carrier can use to define the claim before the adjuster has inspected anything.

Pull the declarations page before calling. It contains the policy number, named insured, coverage limits, and deductible structure.

Have ready: policy number and declarations page, date of loss (the storm date, not the discovery date), contact information, and a one-phrase damage description (hail, wind, or storm damage) — no estimates or dollar figures.

Request before ending the call: claim number, name and direct contact for the assigned adjuster, estimated first-contact timeframe, and the carrier’s claims department mailing address. The claim number is the only identifier that matters from this point forward.

Do not estimate the damage amount, speculate on cause, or agree to a recorded statement without understanding its purpose. A homeowner has the right to decline a recorded statement until they have reviewed their policy. [Colorado Division of Insurance homeowner claim filing.]

Filing Deadlines and the Sworn Proof of Loss

Most homeowners policies require filing within one year of the date of loss, but the exact window is policy-specific. Read the declarations page.

The sworn proof of loss is a separate document a formal written statement, signed under oath, detailing the damage and claimed value. When carriers request it, the submission window is typically 60 days. Failure to submit within that window can void the claim under standard HO-3 policy language. Complete it using the contractor’s inspection report and the adjuster’s Xactimate scope.

Step 3: Adjuster Assignment and What Their Role Actually Is

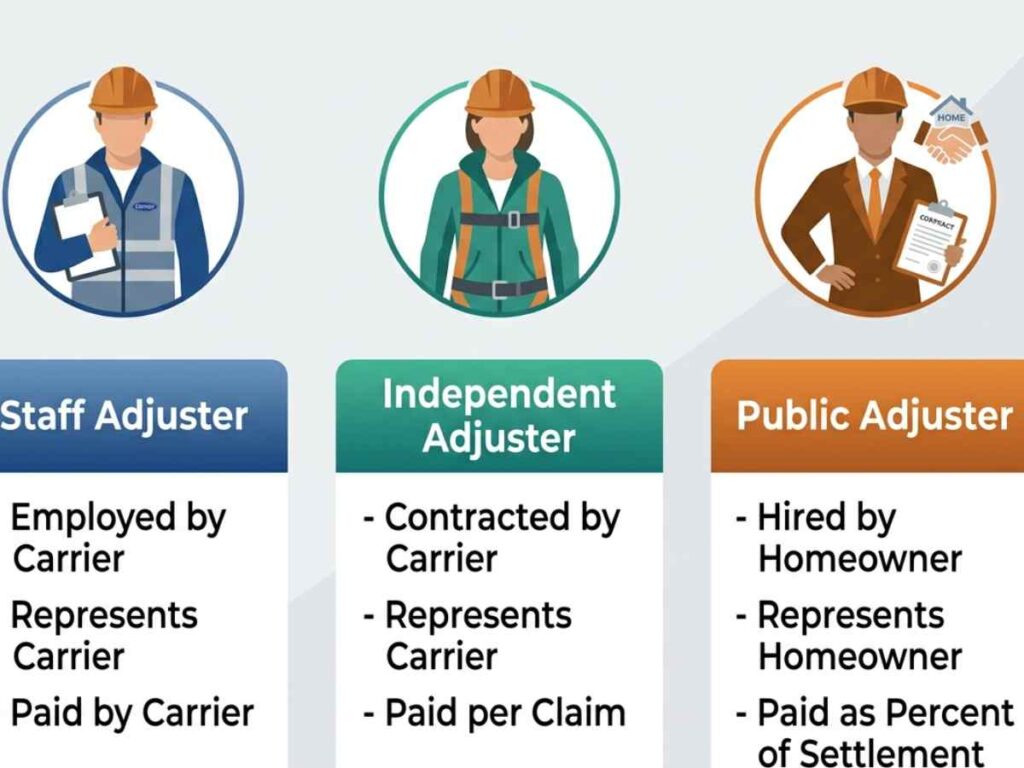

The carrier assigns an insurance adjuster either a staff adjuster employed by the carrier or an independent adjuster contracted by the carrier to inspect the roof and write the scope of loss. Both represent the carrier, not the homeowner. A public adjuster is a third type, hired by and representing the homeowner.

A staff adjuster is a carrier employee, applying the carrier’s internal guidelines with full scope-of-loss authority. An independent adjuster is contracted per claim and is common after major Metro Denver hail events when carrier staff capacity cannot keep pace. Their scope carries the same weight. A public adjuster is licensed by the Colorado Division of Insurance, hired by the homeowner, and paid as a percentage of the final settlement. They are worth considering on large claims or when a scope dispute exceeds what the homeowner can navigate alone.

| Staff Adjuster | Independent Adjuster | Public Adjuster | |

|---|---|---|---|

| Employed by | Insurance carrier | Third-party firm | Homeowner |

| Paid by | Insurance carrier | Insurance carrier | Homeowner (% of settlement) |

| Represents | Carrier | Carrier | Homeowner |

| Scope of loss authority | Yes | Yes | No (advocates only) |

| Licensed by Colorado DOI | Yes | Yes | Yes |

| Common after Metro Denver hail | Less common | Common post-storm surge | Optional, homeowner-initiated |

In Metro Denver, scheduling windows after a widespread hail event can run two to four weeks from assignment to inspection. When the adjuster calls to schedule, immediately notify the contractor the contractor needs to be on the roof at the same time. The contractor’s role during the adjuster inspection is to document what the adjuster counts and what they skip, point out damage on slopes the adjuster may not prioritize, raise soft-metal evidence, and create a contemporaneous record of what was disputed and agreed.

Step 4: The Adjuster Inspection and Xactimate Scope of Loss

The adjuster inspects the roof, measures the field, counts hail impacts on marked test squares, and enters findings into Xactimate the line-item estimating software insurance carriers use to price repairs. The resulting scope of loss report drives the payout.

Xactimate is published by XACT ware, a Verisk company, and is the industry standard across carriers and adjusters in Colorado. It prices work by line item tear-off, underlayment, drip edge, field shingles, ridge cap, flashing with regional unit pricing updated on a cycle. [ Xactimate pricing update cycle, Verisk documentation.] When Metro Denver pricing lags current market rates after material inflation, that gap becomes the basis for a supplement request.

What the Adjuster Does on the Roof

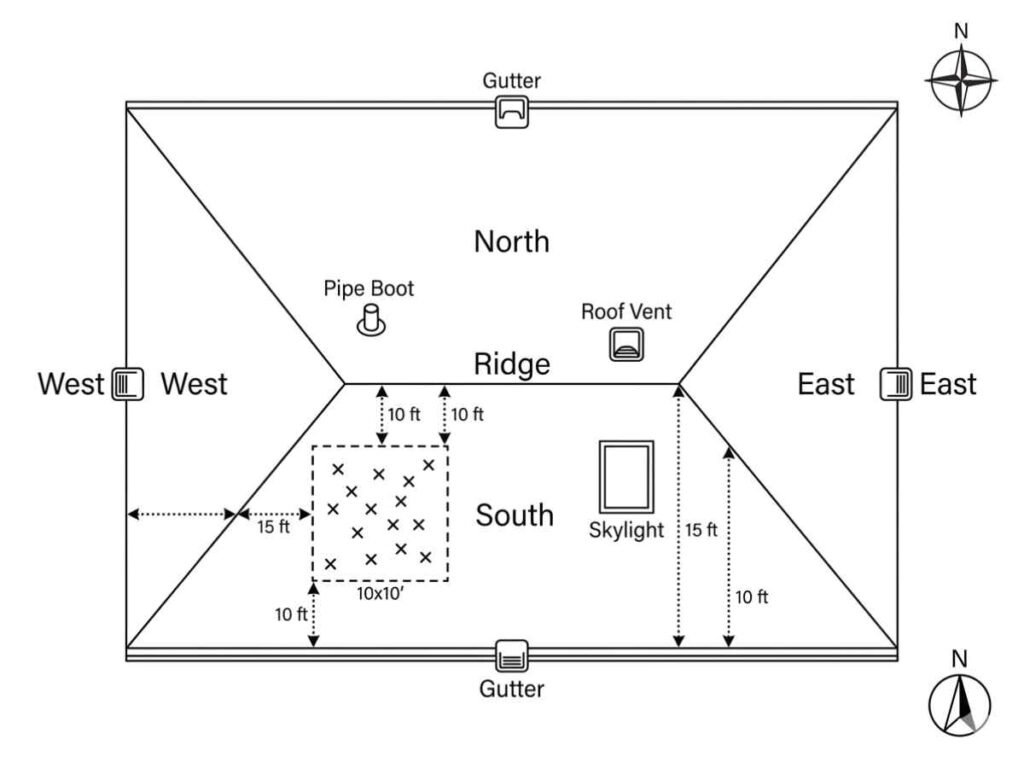

The adjuster identifies a representative test area, typically a 10-by-10-foot section, and chalk-marks hail impact sites within that square. The impact count per slope is the core data point determining whether a slope meets the carrier’s qualifying threshold. Slopes that do not meet the threshold may be excluded entirely. The contractor must be present on every slope, not just the ones the adjuster prioritizes.

After test squares, the adjuster measures total square footage, slope count, pitch, and accessory inventory (vents, skylights, chimneys, pipe boots). A contractor present can flag measurement discrepancies in real time before the scope is written.

The full on-roof sequence: access each slope and identify the test square, chalk-mark confirmed impacts, count impacts per slope against the qualifying threshold, measure the field and accessories, document soft-metal surfaces, and note pre-existing conditions. Pre-existing condition notations are the mechanism carriers use to reduce payout on older roofs a contractor present can respond during the inspection rather than after the scope is issued.

Partial Scope vs Full Replacement Scope

A partial scope identifies specific slopes with qualifying damage and prices repair on those only. A full replacement scope covers the entire field because the damage pattern, material age, or matching standard requires it. Whether a hailstorm with damage on three of five slopes triggers partial or full replacement depends on impact counts, undamaged slope condition, and whether the policy requires matching materials when any portion is replaced. Colorado’s matching standard under SB 38 is covered in Step 6.

Step 5: Scope of Loss, ACV Payment, and the Supplement Process

After the scope of loss is approved, the carrier issues an initial ACV payment the replacement cost minus depreciation and the deductible. If the scope misses items the contractor identifies, the contractor submits a supplement with documentation and Xactimate line items, and the carrier issues a supplemental payment.

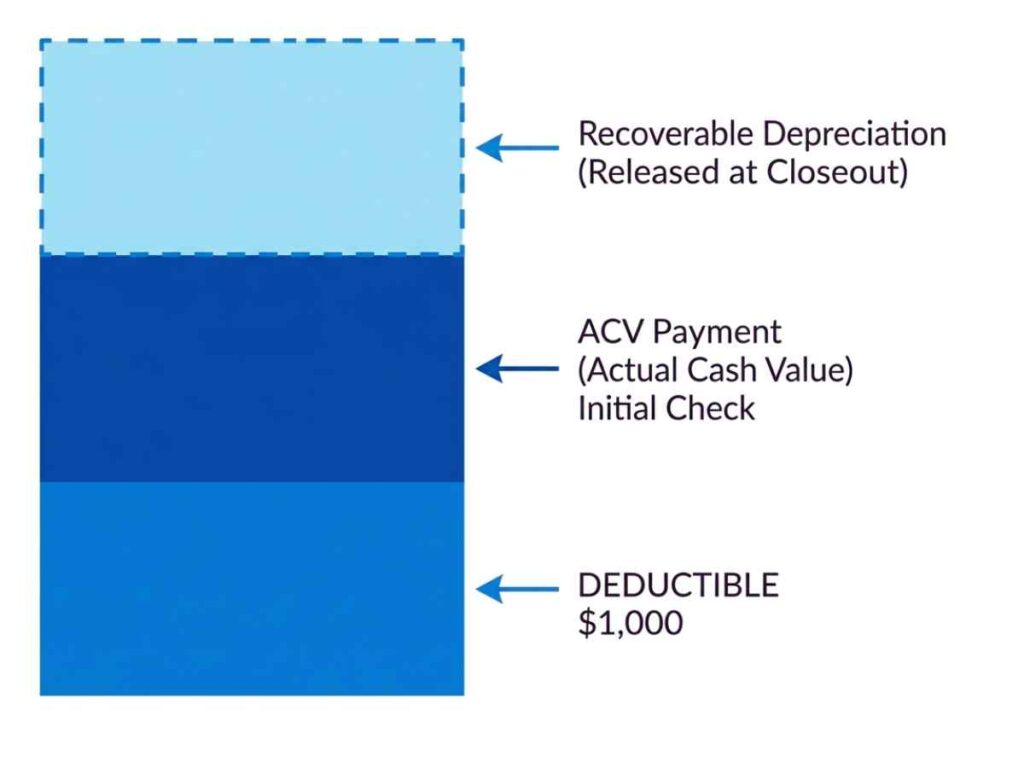

Actual Cash Value vs Replacement Cost Value

Actual cash value is what the roof is worth today, accounting for age and condition. Replacement cost value is what it costs to replace with new materials of like kind and quality. The gap is depreciation. On a 15-year-old asphalt shingle roof in Metro Denver, that gap typically represents 30 to 50 percent of replacement cost.

| Actual Cash Value (ACV) | Replacement Cost Value (RCV) | |

|---|---|---|

| Definition | Replacement cost minus depreciation | Full cost to replace with like kind and quality |

| When paid | After scope approval, before work | After work completion and closeout |

| Depreciation applied | Yes | No; recovered at closeout |

| Deductible subtracted | Yes | Already subtracted from ACV |

| Requires proof of completion | No | Yes; certificate and final invoice |

| Policy type required | Standard HO-3 | RCV endorsement required |

The RCV endorsement is written into the policy. Homeowners on ACV-only policies receive the depreciated value as the final payment regardless of whether the roof is replaced there is no second check.

How Depreciation Works and How the Deductible Is Subtracted

Depreciation is calculated based on roof age, material, and the carrier’s schedule. A 10-year-old asphalt roof with a 25-year lifespan has used roughly 40 percent of its serviceable life, and that percentage is applied to replacement cost to arrive at ACV. Recoverable depreciation is released when the contractor submits the certificate of completion and final invoice. Non-recoverable depreciation is the portion the carrier withholds permanently.

The deductible comes off the top of the ACV payment. On a $18,000 replacement with $4,000 depreciation and a $2,500 flat deductible, the initial ACV payment is $11,500, and the recoverable $4,000 is paid after completion.

Colorado hail market policies commonly carry a percentage wind and hail deductible rather than a flat one. It is calculated as a percentage of the dwelling coverage limit, not the claim. On a home with $400,000 dwelling coverage and a 2 percent deductible, the deductible is $8,000 regardless of claim size. [Percentage wind/hail deductible prevalence in Colorado market.] Calculate it from the declarations page before filing.

What Qualifies for a Supplement

Four categories generate most supplement requests. Missed slopes or accessories when the adjuster did not count qualifying impacts or omitted items like pipe boots and skylight flashing. Hidden damage discovered during tear-off when soft decking, water damage, or rotted sheathing is exposed and photographed. Code-required upgrades are the most consistent source IRC R905 governs residential roof covering and is adopted across Metro Denver, requiring ice and water shield at eaves and valleys, drip edge on rakes and eaves, and specific underlayment standards. The contractor submits a supplement with the code citation and Xactimate line items. [IRC R905 adoption across Denver, Aurora, Lakewood, Centennial, Arvada.] Price escalation applies when Xactimate regional pricing is below the contractor’s current supplier cost, documented with invoices.

Each supplement requires a written description, photographs, Xactimate line items, and where applicable the code citation. Simple supplements typically resolve within two to three weeks; complex supplements involving decking or scope disputes can extend four to six weeks.

Step 6: Contractor Selection and Colorado SB 38 Requirements

Colorado Senate Bill 38, codified as CRS 6-22-101 through 6-22-105 and known as the Residential Roofing Bill, governs every roofing contract tied to an insurance claim in Colorado. It gives homeowners a 72-hour contract rescission right after insurer denial, prohibits contractors from paying, waiving, or absorbing deductibles, and requires specific written disclosures. [CRS 6-22 text and any 2024-2026 amendments.]

The statute exists because Colorado’s hail frequency creates a predictable surge of out-of-state and opportunistic contractors after storms, historically using deductible waiving and high-pressure tactics that left homeowners with voided contracts and fraud exposure.

The 72-Hour Rescission Right

SB 38 gives homeowners the right to cancel a roofing contract within 72 hours of receiving written notice that the insurance claim has been denied. The window runs from the date of written denial, not verbal notice, and rescission must be submitted in writing.

The Deductible Waiving Prohibition and Matching

SB 38 prohibits any roofing contractor from paying, waiving, absorbing, or rebating a homeowner’s insurance deductible through any mechanism. This is a statutory prohibition under CRS 6-22-105, not a guideline. The prohibition covers the statutory matching deductible practice: a contractor quoting the job to match the insurance scope exactly, then absorbing the deductible by inflating a line item, issuing a post-completion rebate, or pricing the work net of the deductible. All three are prohibited. [CRS 6-22-105 penalty language and enforcement mechanism.] A scope inflated to absorb a deductible is a misrepresentation that can void the claim and leave the homeowner liable for the inflated payment.

Required Contract Disclosures

A SB 38-compliant contract must include the contractor’s name, address, and contact information; the scope of work in sufficient detail; the total contract price and payment schedule; written notice of the 72-hour rescission right; and a statement that the contractor will not pay, waive, or absorb the deductible. A contract missing these disclosures should not be signed.

How to Verify a Contractor

Verification is non-optional. Confirm Colorado Secretary of State business registration. Verify municipal licensing Denver, Aurora, Lakewood, Centennial, and Arvada each have their own contractor registration requirements. Request liability insurance and workers’ compensation certificates before signing. A contractor without current liability or workers’ comp coverage leaves the homeowner exposed to property damage and crew injury claims.

Red Flags

Door-to-door solicitors arriving within days of a storm pressuring for an immediate signature is a consistent SB 38 non-compliance pattern. “Free roof” language in any form is a direct violation of the deductible waiving prohibition a roof replacement paid by insurance still requires the deductible. Promises to cover, match, or absorb the deductible are the clearest indicator of non-compliance. [Colorado Attorney General consumer protection guidance on roofing fraud.]

Step 7: Work Authorization and the Start of Replacement

Once the ACV payment is issued and the contractor is selected, the homeowner signs a work authorization agreement, selects shingle product and color, and the contractor pulls the municipal permit and schedules tear-off. Most Metro Denver replacements take one to three days of active work.

What the Work Authorization Must Contain

Under SB 38, the work authorization must include the contractor’s full business name and contact information, complete scope of work tied to the insurance scope of loss, total contract price and payment schedule, material specifications (manufacturer, product line, color), and the written rescission notice required by CRS 6-22-101. Review the agreement against the adjuster’s scope of loss line for line before signing.

Material Selection and Manufacturer Warranty

Shingle selection determines the manufacturer warranty available. Most manufacturers offer tiered coverage: a standard product carries a limited warranty, a premium or impact-resistant product carries enhanced coverage. The contractor’s installer certification status affects the warranty tier a non-certified installer cannot offer the highest tier regardless of product.

Class 4 impact-resistant shingles carry an additional consideration. Under CRS 10-4-110.8, insurers offering Colorado homeowners policies must offer premium discounts for Class 4 roofing materials. The homeowner notifies the carrier after installation and requests the discount it is not automatic.

Permits Across Metro Denver

A building permit is required for roof replacements in every Metro Denver municipality. The contractor pulls it before work begins. Unpermitted work creates inspection complications and can affect manufacturer warranties, carrier closeout requirements, and resale title searches. Permit requirements and fees vary across Denver, Aurora, Lakewood, Centennial, and Arvada.

Scheduling and Tear-Off Day

Metro Denver hail season runs April through September. A claim approved during active season may face a two- to four-week scheduling window. Off-season claims typically schedule within one to two weeks. After major regional hail events, shingle supply from regional distributors can tighten as multiple contractors order simultaneously.

A standard residential crew runs four to six workers with a dump trailer or roll-off in the driveway. The homeowner does not need to be present. Before the crew arrives, move vehicles, remove items from interior walls (vibration can dislodge frames in homes with vaulted ceilings or older plaster), and identify landscaping to protect. Tear-off exposes the decking if soft spots, water damage, or rot are found, the contractor photographs and submits a supplement before replacing those sections.

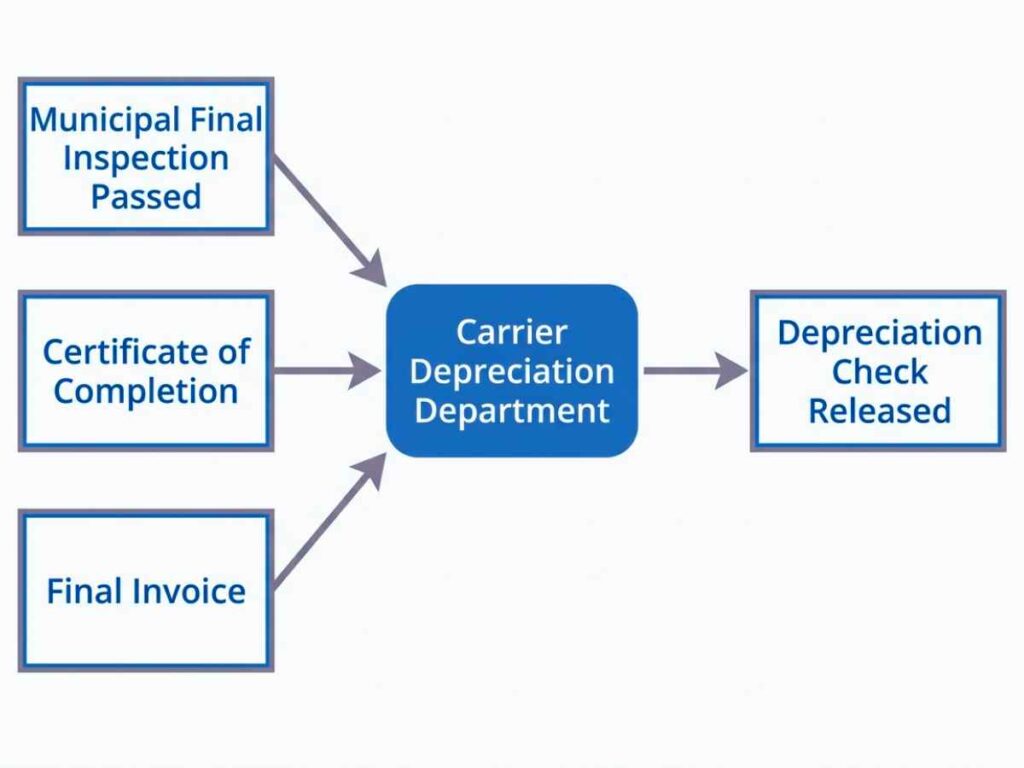

Step 8: Completion, Depreciation Recovery, and Final Payment

After the roof is finished and the municipal inspection passes, the contractor submits a certificate of completion and final invoice to the carrier. The carrier then releases the recoverable depreciation as a final payment. Without submitting this closeout documentation, the homeowner forfeits the depreciation portion of the claim.

What Triggers the Depreciation Release

Three things must be in place. The municipal final inspection must be complete and passed the inspector’s sign-off confirms the work meets local code. The certificate of completion must be submitted to the carrier’s depreciation department, not the general claims line. The final invoice must accompany it and match the approved scope.

What the Contractor Provides for Closeout

The contractor’s closeout package should contain the certificate of completion, final invoice tied to the approved scope, permit closeout documentation showing the final inspection passed, and manufacturer warranty documentation. A contractor who delivers only the invoice is leaving the homeowner to assemble the rest independently.

Why Homeowners Forfeit the Depreciation Payment

Recoverable depreciation is often the larger portion of the total claim on a $20,000 replacement with $6,000 in held depreciation, the final payment is 30 percent of the total. Standard HO-3 policies require completion and closeout submission within a defined window after ACV payment, typically one to two years. [HO-3 depreciation recovery submission window.] Homeowners who cash the ACV check and delay repair often miss the window without realizing the depreciation payment existed.

Timeline and Mortgage Endorsement

Metro Denver depreciation check turnaround typically runs two to four weeks after complete submission. Follow up seven to ten days after submission to confirm receipt and routing submissions sent to the general claims line rather than the depreciation department can sit unprocessed for weeks.

When the claim check exceeds the carrier’s single-signer threshold, the mortgage company is listed as a co-payee. The lender reviews documentation, confirms work was completed, and endorses the check before returning it. Mortgage servicer endorsement in Metro Denver typically runs one to three weeks. Contact the servicer before submitting the closeout package to understand documentation requirements.

Keeping the Insurance Money Without Repairing: What Actually Happens

A Colorado homeowner can cash the ACV check without completing repairs, but the carrier will not release the recoverable depreciation, and the policy may exclude the same damage from future claims. The unrepaired roof also risks non-renewal at the next policy term.

Standard HO-3 policy language typically excludes future claims for damage that is the same as, or directly caused by, unrepaired prior damage. If the roof sustains additional hail damage and the adjuster identifies the pre-existing unrepaired condition, the carrier can attribute a portion of the new damage to the prior loss and reduce or deny that portion.

Carrier non-renewal is a separate risk. A property with documented unrepaired storm damage is a known liability, and in Colorado’s hail markets that is a straightforward justification for non-renewal at the next term.

For homeowners with an active mortgage, the decision may not be available. When the check exceeds the servicer’s single-signer threshold, the homeowner cannot cash a co-payee check without endorsement, and the servicer will not endorse without confirming repair. The servicer typically releases proceeds in draws tied to verified completion milestones. [Colorado mortgage servicer insurance claim disbursement guidelines.]

Consequences of not repairing:

- Recoverable depreciation forfeited permanently

- Future claims for the same or related damage may be excluded under standard HO-3 language

- Carrier non-renewal at the next policy term is a documented risk

- Mortgage servicer co-payee requirements may prevent accessing the check without completing repair

- The unrepaired roof continues to deteriorate, affecting insurability and resale value

When to File a Roof Insurance Claim in Colorado vs When to Wait

File the claim when a licensed contractor confirms qualifying hail or wind damage that exceeds the deductible and the loss is within the policy’s filing window. Wait or skip filing when the damage is cosmetic only, when the estimated scope is at or below the deductible, or when the roof is approaching end of service life and the carrier has flagged it for non-renewal after prior claims.

Filing creates a record on the property’s claim history that affects premium calculations and non-renewal risk. A contractor inspection and a claim are two separate decisions the inspection itself does not require a claim to follow.

| Decision Factor | File the Claim | Wait or Skip Filing |

|---|---|---|

| Damage type | Contractor confirms qualifying functional damage: hail bruising, granule displacement, wind uplift | Cosmetic only: surface marks, minor granule loss |

| Deductible threshold | Estimated scope exceeds deductible by meaningful margin | Scope at or below deductible |

| Roof age and coverage | Mid-life with RCV; not flagged for ACV conversion | Near end of life, shifted to ACV-only, or prior non-renewal warning |

| Claim history | No prior claims or one within five years | Two or more within five years; flagged for review |

| Filing window | Within policy window, typically one year from loss | Window passed or too close |

| Deductible type | Flat deductible low relative to scope | Percentage wind/hail deductible exceeds or matches scope |

The Deductible Threshold Calculation

Flat deductibles are straightforward: a $2,500 deductible on a $14,000 scope produces an $11,500 net before depreciation. Percentage wind/hail deductibles require different math — on a home with $350,000 dwelling coverage and a 2 percent deductible, the deductible is $7,000 regardless of scope size, so a $12,000 scope produces a $5,000 net or less. Calculate it from the declarations page before calling.

How Claim History Affects the Decision

Colorado carriers manage claim exposure differently than lower-frequency markets. A property with two or more hail claims within five years is a known risk. Premium increases are policy-specific, but claim history is a factor in renewal underwriting that gains weight with each additional claim.

Non-renewal is the more significant risk. In Colorado’s hail markets, carriers have non-renewed at a rate that has drawn Colorado Division of Insurance attention. [Rocky Mountain Insurance Information Association non-renewal reporting.]

The Policy Filing Window

Most policies require filing within one year of the date of loss. Some allow two years; some require six months from discovery. A claim filed outside the window is denied on timeliness grounds regardless of damage validity.

When a Paid Inspection Without Filing Is the Right Move

A contractor inspection does not require a claim to follow. When the estimated scope is close to the deductible, a paid inspection produces documentation without opening a claim record. When the roof is near end of life and the carrier has shifted to ACV-only, an inspection establishes the current condition for the homeowner’s records. When claim history is already elevated, a paid inspection gives the homeowner information to make a calibrated decision rather than filing reflexively.

Older Roofs and Carrier Coverage Changes in Colorado

Homeowners insurance in Colorado generally covers an older roof, but many carriers have shifted roofs older than 15 to 20 years to ACV-only coverage, and some now exclude roofs beyond a set age from new applications entirely. The exact threshold is on the declarations page.

Roofs under 10 years typically qualify for full RCV without restriction. Roofs 10 to 15 years old may qualify with conditions including impact-resistant material requirements. Roofs older than 15 to 20 years are increasingly written ACV-only. [Colorado carrier roof age threshold ranges against Colorado Division of Insurance market conduct reports.]

An ACV-only endorsement changes the claim math significantly. On a 20-year-old asphalt roof with a 25-year lifespan, the carrier may value remaining serviceable life at 20 percent of replacement cost on a $22,000 replacement, the homeowner covers the remaining 80 percent out of pocket.

The shift from RCV to ACV-only does not always happen at initial underwriting. Colorado carriers have added roof-age endorsements at renewal on policies that previously carried RCV, and the trend has accelerated along the I-25 and E-470 corridors where storm frequency is highest.

A homeowner past the carrier’s age threshold has three options: shop comparative quotes with the current roof age disclosed (some carriers offer more favorable thresholds), request an underwriting inspection (some carriers will modify coverage if a current inspection confirms good condition), or consider a pre-emptive replacement (a new Class 4 impact-resistant roof resets the age clock, qualifies for the CRS 10-4-110.8 premium discount, and resets coverage from ACV-only back to RCV eligibility). [standard ACV-only endorsement language in Colorado HO-3 policies.]

What to check on the declarations page: roof age schedule or roof payment schedule endorsement, ACV endorsement for roof, cosmetic damage exclusion, wind and hail deductible type and percentage with current dwelling coverage limit, and the policy renewal and endorsement effective dates. If the page does not clearly identify the roof’s coverage structure, call the carrier and ask directly whether the roof is on RCV or ACV-only terms.

What Colorado Homeowners Should Do Before the Next Hail Season

The claim process is easier to navigate when the groundwork is already in place. Most of the decisions that create problems mid-claim are ones the homeowner could have resolved before a storm arrived.

Pull the declarations page and read it. Confirm whether the roof is on RCV or ACV-only terms. Calculate the wind and hail deductible against the current dwelling coverage limit. Note the policy filing window. None of this takes more than 20 minutes and it eliminates the most common sources of claim confusion.

Schedule a condition inspection if the roof is more than 10 years old. A current inspection establishes the roof’s documented condition before storm season. If damage occurs, the pre-storm inspection report is the baseline that ties new damage to the new loss event rather than leaving the carrier room to attribute it to prior wear. It also tells the homeowner whether the roof is approaching the age threshold where the carrier is likely to shift coverage terms at the next renewal.

Verify the contractor before the storm happens. A contractor selected under pressure after a major hail event is a contractor selected without adequate verification time. Checking Colorado Secretary of State registration, confirming municipal licensing in the relevant jurisdiction, and requesting liability and workers’ compensation certificates takes less time before a storm than after one.

The claim process rewards preparation. Every step that is done in advance is one fewer decision made under pressure.

Recent Comments