Colorado homeowners who install Class 4 impact-resistant shingles can qualify for premium discounts of 15% to 30% on the dwelling coverage portion of their homeowner policy. CRS 10-4-110.8 requires Colorado insurers to factor impact-resistant roofing materials into their premium rate structures, and that rate filing framework is how the discount reaches your premium.

In June 2026, Governor Polis signed SB26-155 into law. The bill creates the Strengthen Colorado Homes Enterprise within the Division of Insurance. Starting no sooner than January 2027, insurers must prove in their rate filings that savings from resilient roof installations are reaching policyholders, making the discount enforceable rather than voluntary.

The discount is not automatic. Homeowners from Metro Denver south through Castle Rock and Parker along the Front Range hail corridor need three things: qualifying Class 4 materials on the roof, a closed building permit, and the manufacturer’s certification submitted to their carrier. This guide covers what the statute requires, how the Class 4 rating works, how much the discount saves, and how to request the reduction.

What Does CRS 10-4-110.8 Require for Impact-Resistant Roofing?

Colorado insurers who write homeowner policies must incorporate impact-resistant roofing materials into their rate structures under §10-4-110.8. The statute is one of the broadest in Title 10, Article 4 of the Colorado Revised Statutes, covering prohibited insurer practices, replacement cost estimate requirements, additional living expense coverage, and policy readability standards. The roofing discount is one component inside that larger framework.

No single subsection mandates a specific discount percentage. The discount operates through rate filings: when an insurer calculates premiums for a Colorado homeowner policy, impact-resistant materials must be factored into the rate. Most competitor pages across the Front Range treat §10-4-110.8 as though it contains explicit discount language, which overstates what the statute provides. The discount is a rate structure outcome, not a statutory command.

Governor Polis signed SB26-155 on June 8, 2026, creating the Strengthen Colorado Homes Enterprise inside the Division of Insurance, the regulatory arm of DORA. Starting no sooner than January 1, 2027, insurers offering multiperil homeowner policies must demonstrate in their rate filings that savings from resilient roof installations reach policyholders as discounts or reduced premiums. The Enterprise collects an annual fee of 0.5% of total premium from admitted insurers, giving it a dedicated budget to audit whether carriers are actually passing savings through.

“Resilient roof systems” is a defined term under SB26-155. It covers Class 4 impact-resistant shingles but extends beyond them. At least 90% of the Enterprise’s fee revenue goes to grants for homeowners retrofitting with qualifying systems, and the specific standards defining what qualifies will be set through DOI rulemaking rather than locked into the bill text.

How Does the UL 2218 Class 4 Test Work?

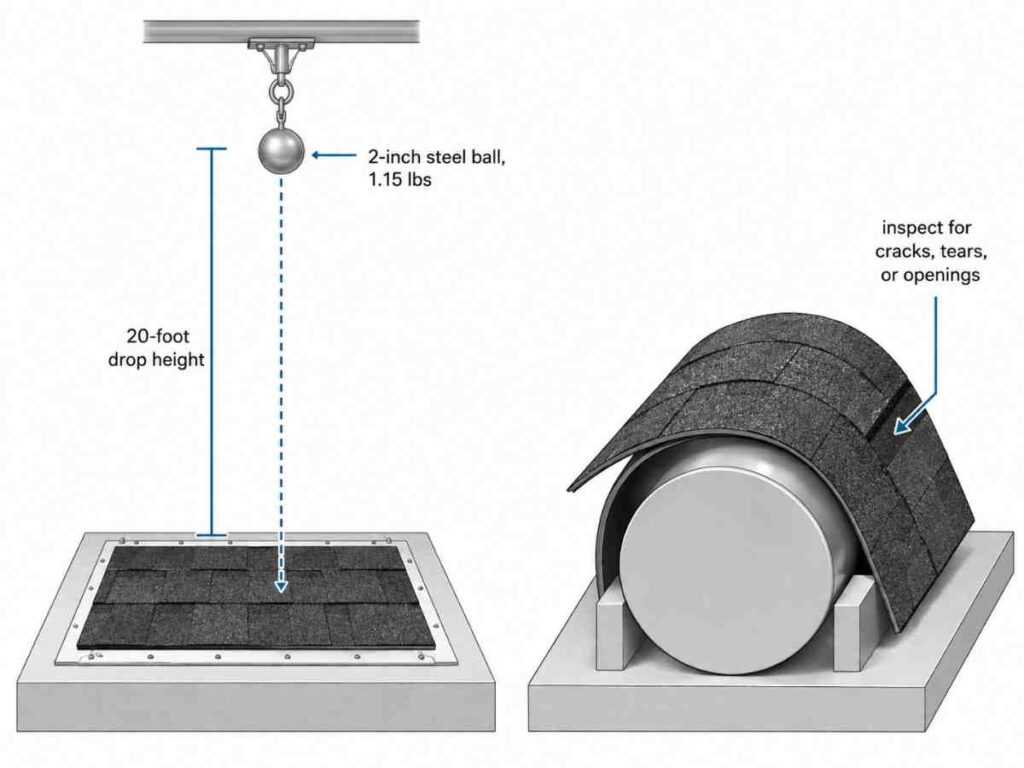

A shingle earns the Class 4 rating by surviving two direct strikes from a 2-inch steel ball weighing 1.15 pounds, dropped from 20 feet onto a mounted test deck. After both impacts, the shingle is flipped and bent over a curved form called a mandrel. No cracks, tears, or openings on the back surface means a pass.

The UL 2218 scale runs four levels. Class 1 uses a 1.25-inch ball from 12 feet, Class 2 a 1.5-inch ball from 14 feet, Class 3 a 1.75-inch ball from 17 feet. Class 4 is the ceiling. UL LLC oversees all testing as an OSHA-recognized Nationally Recognized Testing Laboratory and certifies which products carry each rating.

FM 4473 offers a parallel path using frozen ice balls instead of steel, launched from a compressed air cannon at roughly 76 mph to match the kinetic energy of a same-size hailstone in free fall. Colorado insurers treat FM 4473 Class 4 and UL 2218 Class 4 as equivalent benchmarks when evaluating discount eligibility.

The material technology matters here. SBS-modified asphalt blends styrene-butadiene-styrene rubber polymers into the shingle formulation, absorbing impact energy rather than cracking under it, and that polymer integration is what separates most Class 4 products from standard architectural shingles. The IBHS FORTIFIED Roof program takes a wider view: instead of rating the shingle alone, FORTIFIED certifies the entire roof assembly, evaluating deck attachment, sealed roof deck, and edge metal alongside impact resistance, and some Colorado insurers recognize that designation as an additional or alternative pathway to the premium discount.

Which Colorado Homeowners Qualify for the Discount?

Any Colorado homeowner with a multiperil homeowner insurance policy who installs Class 4 rated roofing materials, obtains a building permit, and notifies their insurer with qualifying documentation can request the premium discount. The discount is not applied automatically. Qualification comes down to three components that must all be in place before the carrier will process the request:

- The installed roofing material carries a manufacturer-certified UL 2218 Class 4 or FM 4473 Class 4 rating.

- A building permit for the roof replacement has been pulled and finalized with the local jurisdiction.

- The homeowner has notified their insurer and submitted the manufacturer’s certification letter along with a contractor invoice specifying the Class 4 product installed.

The discount applies to the dwelling coverage portion of the policy, not the total annual premium. Homeowners should contact their carrier before installation to confirm what documentation format the insurer requires. Those who already have a qualifying Class 4 roof installed can request the discount retroactively by providing the same three components: manufacturer certification, closed permit, and contractor invoice specifying the product.

The request must come from the homeowner. Carriers do not scan permit records or monitor roof replacements. Permit requirements and fees vary across Metro Denver municipalities, and the differences matter:

- Denver, Aurora, and Lakewood each set their own permit fee schedules and inspection timelines.

- Castle Rock and Parker operate under Douglas County jurisdiction with separate application processes.

- Centennial follows Arapahoe County permitting rules, which differ from both Denver and Douglas County procedures.

Skipping the permit creates three problems. Manufacturer warranties on Class 4 products often require proof of permitted installation for coverage to activate. Carriers processing hail damage claims may delay or deny closeout on unpermitted roofs, leaving the homeowner to resolve the documentation gap before the claim closes. Title searches during resale can surface unpermitted work as a defect. The contractor is responsible for pulling the permit before work begins, not the homeowner.

How Much Can Colorado Homeowners Save With Class 4 Shingles?

Colorado insurers offer premium discounts of 15% to 30% on the dwelling coverage portion for homes with verified Class 4 roofing. The exact percentage depends on three variables: the carrier, the policy structure, and the property’s geographic hail risk zone.

| Factor | Standard Architectural | Class 4 Impact-Resistant |

|---|---|---|

| Material cost per 100 sq ft | Baseline | 10% to 20% premium (~$50 more per 100 sq ft) |

| Total material cost premium (typical Metro Denver residential roof) | Baseline | ~$1,000 to $2,000 above standard |

| Annual insurance savings (dwelling coverage portion) | None | ~$400 to $700 |

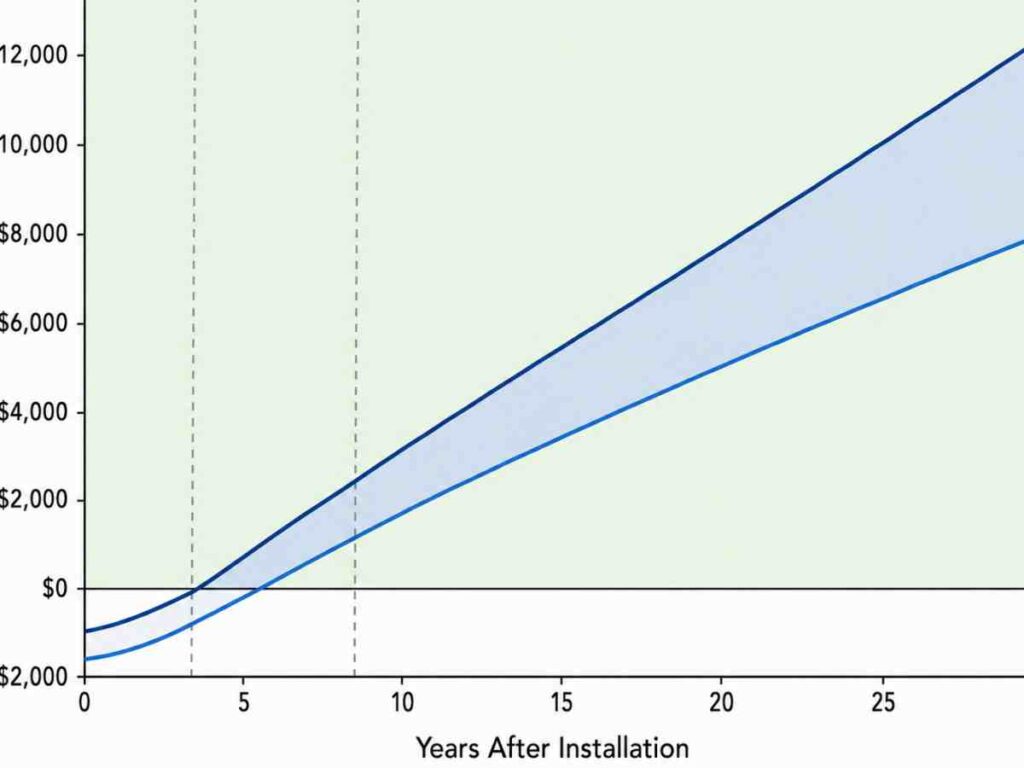

| Breakeven on material cost premium | N/A | 3 to 7 years |

| Net savings over 30-year roof lifespan | N/A | 23 to 27 years of annual discount beyond breakeven |

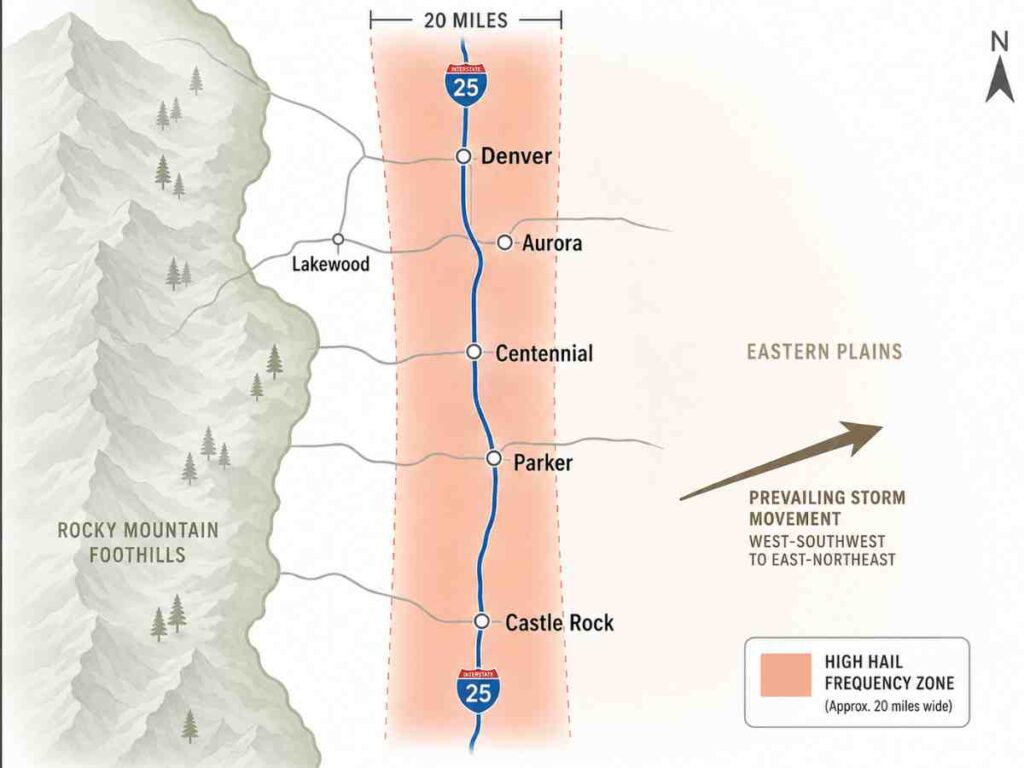

A homeowner carrying $400,000 in dwelling coverage on a $2,400 annual premium could see the dwelling-allocated portion discounted by 15% to 30%, producing $360 to $720 in annual savings depending on carrier and policy structure. State Farm, USAA, Farmers, and Allstate all offer discount programs for Colorado properties with qualifying Class 4 materials. Percentages vary. Some carriers tier their discount by hail risk zone, offering higher reductions for properties along the I-25 corridor from Castle Rock through Denver where claim frequency is highest.

The material cost premium over standard architectural shingles adds roughly $1,000 to $2,000 on a typical Metro Denver residential roof. At the savings ranges in the table above, the additional material cost is recovered within the breakeven window, and every year after that is net return.

That net return compounds. A Class 4 roof with a 30-year manufacturer lifespan generates 23 to 27 years of annual discount beyond breakeven. On a $500 annual discount, that is $11,500 to $13,500 in cumulative savings over the remaining life of the roof. The homeowner also eliminates one full replacement cycle that a standard architectural shingle on the Front Range would require within 15 to 20 years due to accelerated UV and hail degradation at altitude.

Which Class 4 Shingles Qualify for Colorado Insurance Discounts?

Any asphalt shingle carrying a manufacturer-certified UL 2218 Class 4 or FM 4473 Class 4 rating qualifies for the discount. The brand does not determine eligibility. The certification does. The four most widely installed Class 4 products in Colorado differ in formulation, construction, and warranty terms:

| Product | Manufacturer | Asphalt Technology | Warranty Range |

|---|---|---|---|

| Timberline AS II | GAF | SBS-modified asphalt | 30 years (limited lifetime with conditions) |

| Duration FLEX | Owens Corning | SBS-modified asphalt, different granule adhesion approach | 30 to 50 years (depending on installation tier) |

| Vista AR | Malarkey | Proprietary polymer-modified, rubberized asphalt blend | 30 years (limited lifetime) |

| Presidential Impact | CertainTeed | Multi-layer laminate construction | 50 years (with registered installation) |

The qualifying criterion is the Class 4 certification on the product, not which company manufactured it. Shingles from smaller or regional manufacturers carry the same discount eligibility as long as the UL 2218 or FM 4473 Class 4 rating appears on the manufacturer’s certification letter. That letter is the document the homeowner submits to their carrier.

Homeowners should verify one thing before signing. The specific product being installed must appear on the manufacturer’s current Class 4 certified product list, not a discontinued or reclassified line. Manufacturers update their certified product lists when formulations change, and a product that carried Class 4 certification two years ago may not carry it today. The contractor should confirm the current certification status and provide the letter at project completion.

Why Does the Front Range Hail Corridor Make Class 4 a Financial Decision?

The Colorado Front Range averages 7 to 9 hail days annually between April and September, with insured hail losses regularly exceeding $1 billion per year statewide. The corridor from Denver south through Castle Rock and Parker along I-25 absorbs the highest concentration of those events. May and June are the worst months. Supercell thunderstorms push east off the foothills, cross the I-25 corridor, and lose energy over the eastern plains.

The Division of Insurance has identified hail damage as the number one cost driver of homeowner insurance rates in Colorado. That finding is the actuarial reason the premium discount exists: Class 4 roofs file fewer claims after hailstorms, and fewer claims mean lower loss ratios for carriers writing policies along the Front Range.

Denver sits at 5,280 feet. At that altitude, roofing materials absorb more intense UV radiation than the same products installed in lower-elevation markets. Standard architectural shingles on the Front Range typically show accelerated granule loss and mat deterioration within 15 to 20 years, roughly five to ten years sooner than identical products at sea level. Freeze-thaw cycles between November and March compound the damage: moisture enters micro-fractures created by UV exposure, expands when it freezes, and widens the cracks with each cycle.

SBS-modified asphalt resists both mechanisms. The rubber polymer integration that enables Class 4 impact performance also absorbs UV energy and flexes through freeze-thaw cycles without cracking. A Class 4 roof on the Front Range extends functional life to 30 years or more, eliminating one full replacement cycle that a standard architectural shingle would require within two decades at this altitude.

What Happens if Your Insurer Denies the Class 4 Discount?

A homeowner whose carrier denies the Class 4 discount can file a complaint with the Colorado Division of Insurance through the DORA consumer portal. Starting no sooner than January 2027, SB26-155 requires insurers to demonstrate savings passthrough in their rate filings, giving DOI an auditable paper trail to evaluate denial complaints. Before filing, the homeowner should confirm the documentation is complete:

- The manufacturer’s UL 2218 or FM 4473 Class 4 certification letter, confirming the specific product installed carries the current rating.

- The building permit showing the roof replacement was permitted, inspected, and finalized with the local jurisdiction.

- The contractor invoice specifying the Class 4 product by name and confirming installation is complete.

If all three documents are in order and the carrier still denies the discount, request the denial in writing. The written denial must cite the specific reason. That reason becomes the basis for the DOI complaint.

DOI reviews complaints related to rate application, discount denial, and unfair insurance practices under Title 10. The complaint process is administrative, not legal. Homeowners do not need an attorney to file. The agency evaluates whether the carrier’s rate filing and discount application comply with Colorado insurance regulations, and after January 2027, whether the carrier’s rate filing demonstrates the savings passthrough that SB26-155 requires.

Switching carriers is the other option. Discount percentages vary by insurer, and a homeowner with a verified Class 4 roof can obtain comparative quotes from competing carriers. A carrier that denies or undervalues the discount may simply have a less favorable rate structure for impact-resistant roofing, and a different carrier writing in the same hail risk zone may offer a higher reduction on the same roof.

How to Request the Class 4 Discount From Your Insurance Carrier

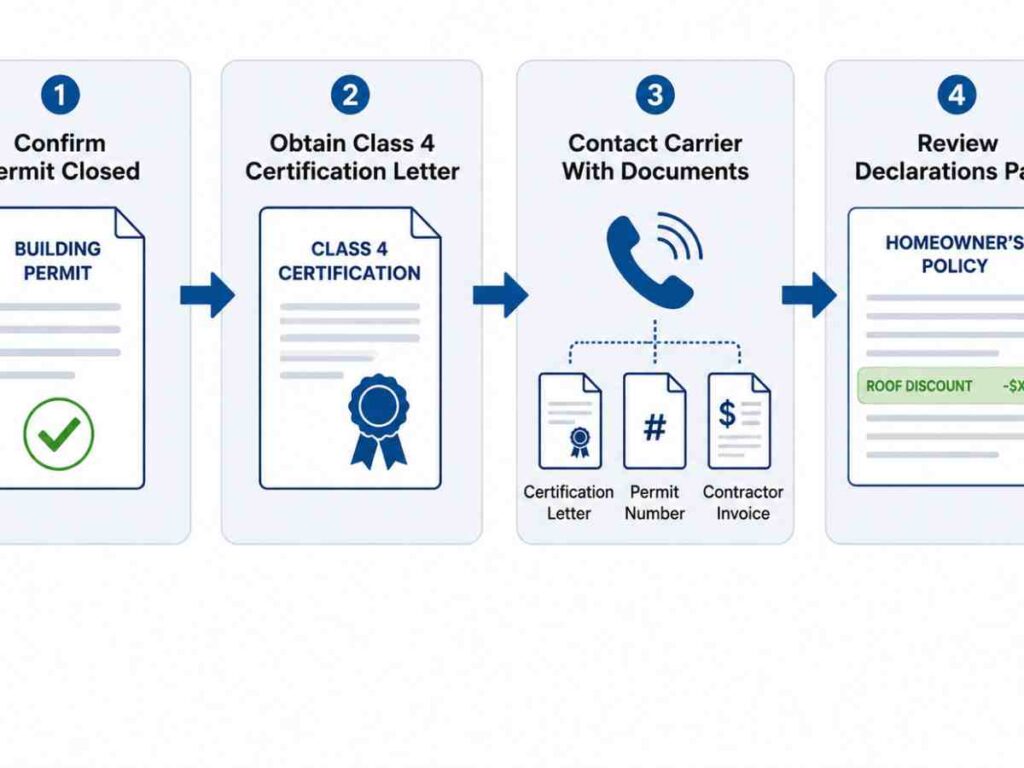

Contact your insurance carrier after the Class 4 roof installation is complete, the building permit is finalized, and you have the manufacturer’s Class 4 certification letter in hand. Request the impact-resistant roofing premium discount on the dwelling coverage portion of your policy. The process follows a specific sequence:

- Confirm the installation is complete and the building permit is closed with the local jurisdiction. Do not contact the carrier until the permit is finalized.

- Obtain the manufacturer’s UL 2218 or FM 4473 Class 4 certification letter from your contractor. The letter must name the specific product installed and confirm its current Class 4 rating.

- Call your carrier and request the impact-resistant roofing discount. Provide three documents: the certification letter, the closed building permit number, and the contractor invoice specifying the Class 4 product by name.

- After the carrier processes the request, review your next declarations page to confirm the discount appears and note the effective date.

The declarations page is the summary document your carrier issues with each policy term showing coverages, limits, and applied discounts. A discount that does not appear on the first declarations page after the request typically means the carrier logged it for the next renewal cycle rather than the current term.

Timing determines when the savings start. Some carriers apply the discount at the next policy renewal rather than mid-term, which means a homeowner who requests the discount in March on a policy that renews in October waits seven months before the rate reduction takes effect. Requesting immediately after installation queues the discount for the earliest possible effective date.

One question remains before the process is complete. The discount percentage may vary by geographic zone within Colorado, and the carrier can confirm which zone applies to the property. Properties along the Front Range hail corridor from Denver south through Castle Rock and Parker may qualify for higher discount percentages than properties in lower-risk areas of the state. Carriers that tier by zone base the differential on claim frequency data, and a homeowner in a high-frequency zone who accepts the default discount without confirming their zone classification may be leaving the upper end of the 15% to 30% range on the table.

Recent Comments